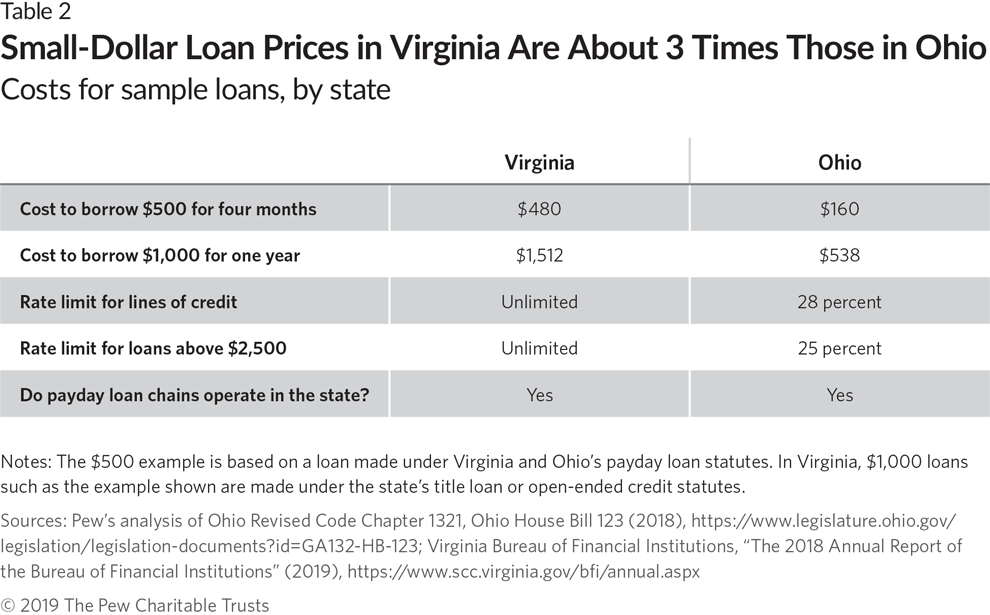

Payday borrowers disproportionately come from poor and minority communities. The teams using the greatest likelihood of having utilized a loan that is payday “those with no four-year college education; house renters; African Us citizens; those making below $40,000 annually; and people who will be divided or divorced,” reports Pew. 71 among these faculties, being African United states could be the solitary strongest predictor: African People in america are 105 % prone to utilize an online payday loan than many other cultural groups. 72

Payday loans online seem to take into account a significant percentage of the payday market, and they’re usually riskier than their offline counterparts. 73 90 per cent of Better Business Bureau complaints about payday loan providers relate solely to online, maybe maybe not storefront, loan providers. 74 they have been connected with higher costs and long run indebtedness. 75 they often times include complex terms and payment structures and may be particularly confusing for customers. 76 And online borrowers report high prices of abusive telephone calls. 77

Online loans that are payday be a gateway to fraudulence.

Online loans that are payday additionally be a gateway to fraudulence. Because online loan providers typically count on electronic usage of borrowers’ bank accounts (in place of a check that is postdated, payday lead generators almost invariably collect customers’ bank account information. This information is often provided recklessly. Nearly a third of online payday borrowers surveyed by Pew stated that their individual or monetary information ended up being offered without their permission. 78 almost as numerous reported unauthorized bank withdrawals regarding the an online cash advance. 79

Federal regulators have actually over and over discovered payday lead generators in the center of sweeping economic fraud operations. In 2014, the Federal Trade Commission (FTC) sued LeapLab, a business that “collected thousands of customer cash advance applications” from lead generators, and then “used the leads to help make huge amount of money in unauthorized debits and charges.” 80 the year that is same in addition it sued CWB Services LLC, which made unauthorized withdrawals from consumers’ bank accounts using information purchased from lead generators.” 81 In 2015, it sued Sequoia One, LLC and Gen X Marketing, two organizations whom bought (or collected) pay day loan leads from lead generators and offered those results in non-lenders whom fraudulently withdrew funds from consumers’ bank reports. 82 likewise, the CFPB sued Hydra Group, which made repeated unauthorized withdrawals from consumers’ bank accounts data that is using from lead generators. 83

Landing Pages and  Affiliates

Affiliates

On the web ads tend to be doorways to landing pages — the internet sites by which customers’ information enters the to generate leads market. Landing pages frequently feature a “call to action” (such as “Get Cash Now!”) that entices consumers to enter information on by themselves into an application in the web web web page. In a few cases, landing pages are run by big, brand-name to generate leads companies like MoneyMutual and LowerMyBills. But, in a lot of cases, “affiliates” — individuals and small enterprises trying to earn money by creating leads — form the leading lines, hosting landing pages and drawing customers in.

Affiliates are conscripts of larger, more lead that is sophisticated businesses. These organizations typically allow it to be simple to join their affiliate system. 38 Some offer catalogs of pre-designed splash page templates and other materials that are creative. (“You don’t need certainly to think of certainly not driving traffic to your website,” boasts one generator that is lead. 39 ) effective affiliates spend heavily in internet marketing, making certain their internet sites ranking highly in serp’s, and creating their sites look trustworthy. 40

End-buyers also score contributes to assist them to gain a competitive side. As an example, relating to a market pamphlet, Liberty University “purchases lots of its most readily useful leads from lovers that offer the exact same contributes to its rivals. To be the university that is first follow through with an eager student, it required the capacity to immediately recognize high-value students — those almost certainly to keep enrolled through graduation. . . . The school’s lead-scoring model instantly categorizes tens and thousands of leads per month”